The Wall Street Journal ran a post over the weekend about a new credit crunch among low income borrowers, noting it is now ‘payback time.’ What they didn’t go into is that their primary interviewee is drowning not on expensive cars loans but student loans. This former student’s debt is far from extraordinary. It is, in fact, tragically ordinary, as student loans have become the 21st century version of indentured servitude.

By Mike Konczal

From The Wall Street Journal, The ‘Democratization of Credit’ Is Over — Now It’s Payback Time. Check out the lead:

NEW YORK — Karen King owes nearly $36,000, more than she’s ever earned in a year. All day long, bill collectors call. She hunts for a second job, sometimes skips meals, and stays with other family members at a grandfather’s crowded apartment, trying to get out of debt and turn her life around.

She largely holds herself at fault. “Years ago, I lived for now. It was so stupid,” the 28-year-old says. “It’s depressing, but I can’t live that life anymore.” Now, she says, “I basically want to live for the future.”

Now go about halfway through.

Her biggest chunk of debt, $26,000, stems from student loans to pay for her two-year associate’s degree from a community college — loans now in the hands of collectors. The remaining $10,000 or so includes old credit-card balances, debt to a store that rents furniture, utility bills and back taxes. Another obligation is $400 a month she contributes to the rent on her grandfather’s two-bedroom apartment, where her mother, uncle and sister also live.

Rolfe Winkler caught this too. In addition to pointing out how the current recession is focused in large part on men, it’s also worthwhile to note that the current recession is devastating the young. Here’s BusinessWeek on “The Lost Generation.”

But let’s go back to the person in question here: How should we judge this young person profiled in the Wall Street Journal? Is going into a large debt load to pay for college the post-Risk-Shift American Dream? Or is it a form of Living For Now, and being irresponsible and short-sited? According to FinAid.org, the average cumulative debt among graduating seniors is about $22,500. She’s ahead of that ($26K/2 years), but what is an acceptable amount of debt to carry to educate yourself? As as Krugman notes, education is a key to our country’s successes. Why should we think of her as irresponsible, instead of someone rationally going into debt peonage, like a 17th century indentured servant, in order to take a small shot at bettering oneself – the new middle class dream?

The New Indentured Servitude

Jeffrey Williams, in Dissent Magazine, wrote Student Debt and The Spirit of Indenture, provocatively referred to student loans as the new form of indentured servitude.

Why is this the new form of indentured servitude? Williams gives some reasons: The prevalence of this debt, especially among the young and the poor/working classes, the transformation from a rounding error amount to a significant burden amount over the past 30 years, the length of term, the idea of mobility and “transport” to a job, debt secured not by property but by personhood, and limited legal recourse. All these characteristics are similar. The limited legal recourse is noteworthy here, since unlike most debt, it isn’t dischargeable under bankruptcy, thus it doesn’t have a natural protection for the consumer receiving credit (a protection, the original synthetic put option, that our Founders were aware of enough to make sure it was provisioned for in the Constitution).

This is not to soft-peddle indentured servitude. Indentured servitude was a violent contract, with physical torture used to coerce labor. As economist DW Galenson noted, “The Company clearly felt that [beaten workers running away] threatened the continued survival of their enterprise, for they reacted forcefully to this crime. In 1612, the colony’s governor dealt firmly with some recaptured laborers: ‘Some he apointed to be hanged. Some burned. Some to be broken upon wheles, others to be staked and some to be shott to death.'” But let’s put on our Galenson Economic Historian googles and think of it as an economic efficiency problem. Indentured servitude, like student loans, are a form of consumption smoothing. And one thing that is needed for consumptions smoothing is good information about the future.

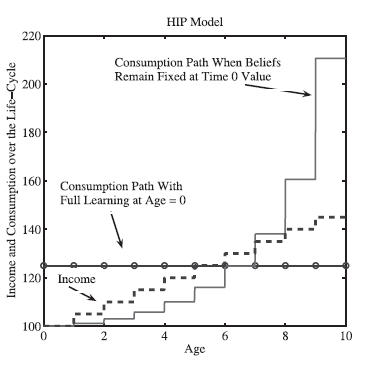

Learning Your Earning

Here’s a graph from University of Minnesota macroeconomist Fatih Guvenen’s Learning Your Earnings:

Think of these two lines as a dial between perfect knowledge and no knowledge. In this model, a consumer who knows what he’ll make over his or her life will consumption smooth (perfect, or ‘full’, knowledge, flat consumption line); one who is uncertain about what will happen next will rationally not. So if you know exactly how much you’ll be making in the future, large loans aren’t really a problem.

Now we are currently asking children, 17, 18 or 19 years old, to try and assess how much of a student loan debt burden they can handle vis-a-vis their future income over their entire lives. But, especially compared to their grandparents, uncertainty is so much greater now. The consumption smoothing line invokes a world where everyone with a college degree will get a stable, solid job with certainty (and your employer will, of course, pick up the health care tab).

The person in the Wall Street Journal article almost certainly had no realistic idea for what would be awaiting her on the other side of the associate’s degree, and she misjudged this terribly. And, from an efficiency point of view, it’s what makes this more perverse than the indentured servitude contract – people under indentured servitude had the job waiting for them. The clock was ticking for the firms who had set up the contract, and they needed to get their value. With student loans, they can sit there for decades, never dischargeable, always getting paid regardless of recession or job market.

Source: Information Clearing House